What is a Project Budget?

A project budget describes the financial and staffing framework that has been approved for executing a project. It defines the upper limit of the resources available to the project team — broken down by cost type, time period, and work package.

The project budget is more than a single number. It is a structured spending plan that shows how much money is allocated for what purpose and when costs are expected to occur. It is released in the project charter and accompanies the project from planning through completion.

An important distinction: the cost plan breaks down expected costs in detail — per work package, resource, and time period. The project budget is the approved financial framework derived from it. The cost plan is the basis for calculation; the budget is the binding upper limit.

In the project management triangle, costs — alongside time and scope — represent one of the three target dimensions. The project budget is the central control instrument for this dimension. Anyone who doesn’t keep the budget under control puts the project goals at risk as a whole.

Why is a Project Budget Important?

Projects without a budget are like a road trip without a full tank — sooner or later you run out. The consequences of missing or inadequate budget planning are well documented: according to a study by the Project Management Institute (PMI), only 62% of projects stay within their planned budget. The remaining 38% exceed it — often because planning was too superficial.

Providing planning certainty. An approved budget gives the project team a clear framework. It answers the question of which resources are actually available — and prevents money from running out mid-project.

Delivering a basis for decisions. Clients and steering committees can only make informed decisions about a project when they know the expected costs. The budget makes the financial dimension transparent and traceable — and is therefore a key input for the cost-benefit analysis.

Detecting deviations early. Only a planned budget makes a plan-vs.-actual comparison possible during the live project. Without a target value, there is no benchmark against which actual costs can be measured. Without a benchmark, there is no early warning.

Forcing prioritization. Limited resources demand focus. What is truly necessary to achieve the project goals? What is merely “nice to have”? The budget makes this discussion concrete and measurable.

Establishing accountability. An approved budget is an agreement between the project manager and the client. It creates responsibility on both sides — and a foundation for project controlling.

Components of a Project Budget

A complete project budget encompasses more than the obvious personnel costs. The following cost types should be considered in budget planning.

Internal personnel costs. Hourly or daily rates of internal employees working on the project. Even if these costs don’t have to be “paid” in some organizations, they tie up real capacity and should be visible in the budget.

External personnel costs. Freelancers, external consultants, temporary workers — all resources brought in from outside that incur direct costs.

Material costs. Materials, software licenses, hardware, infrastructure, prototypes — everything that needs to be procured or rented.

External services. Services from outside providers contracted as a complete package: agencies, specialized firms, laboratories.

Travel and training costs. Business travel, workshops, conferences, and professional development measures required for the project.

Overhead costs. Proportional costs for office space, IT infrastructure, administration — allocated as a flat rate or percentage depending on the organization.

Contingency reserve. A buffer for identified risks whose occurrence would generate additional costs. Rule of thumb: 5–10% of the total budget, depending on the risk profile of the project.

Management reserve (optional). An additional buffer for unknown risks — i.e., events that were not identified in the risk analysis. Typically managed by the client and released only upon request.

In practice, a distinction is often made between the resource budget (for the use of internal capacity) and the financial budget (for material costs, external services, and external expenditures). Together, these make up the complete project budget.

Creating a Project Budget — Step by Step

1. Clarify Project Goals and Scope

Every budget is based on a clear answer to the question: What should the project achieve — and what is out of scope? Without defined project goals and a delineated project scope, any cost estimate is speculation.

Define the project scope as precisely as possible: What results will be delivered? Which requirements are included, and which are explicitly excluded? Because scope creep — the gradual expansion of the project scope — is one of the most common reasons for budget overruns.

2. Define Work Packages and Deliverables

Break the project scope down into concrete work packages. The work breakdown structure (WBS) is the proven tool for this: it decomposes the overall project hierarchically into plannable, estimable units.

The rule is: costs are not estimated at the overall project level, but per work package. The finer the breakdown, the more accurate the estimate — and the lower the risk of overlooking hidden costs.

3. Identify Resources

For each work package, clarify: Who works on it? What materials, tools, or licenses are needed? What external services need to be procured?

Consistently distinguish between internal and external resources — they follow different cost models. And don’t forget the indirect costs: onboarding new team members, training for a new tool, or provisioning additional workstations.

4. Estimate Costs

Estimate the costs for each work package — based on the identified resources and the estimation methods described in the next section. In addition to the magnitude of the costs, their timing is also relevant: when do which costs occur? This is critical for cash flow planning and the later plan-vs.-actual comparison.

A realistic effort estimation is the foundation of every sound budget. Invest sufficient time here — errors in estimation compound across the entire project.

5. Plan for Contingency Reserves

No project runs exactly to plan. Contingency reserves absorb the inevitable deviations without the budget immediately being blown.

The rule of thumb: 5–10% of the total budget as a contingency reserve. The exact amount should be derived from the risk analysis: projects with high technical or organizational risks need more buffer than routine projects. The key is that the reserve is consciously planned and not cut during the approval process.

6. Compile the Budget and Get It Approved

Bring all line items together in one document: individual items per work package and cost type, total amount, timeline of expected expenditures, contingency reserves, and responsibilities. The result is the budget request.

Submit this to the client or steering committee for approval. A well-documented budget with a clearly traceable rationale significantly increases the chances of approval — and gives decision-makers the confidence that the funds will be used wisely.

7. Plan Budget Monitoring

A budget is only useful if it is actively monitored throughout the project. Before the project starts, define:

- Frequency: How often is the plan-vs.-actual comparison performed? (weekly for dynamic projects, monthly for more stable ones)

- Thresholds: At what deviation is escalation triggered? (e.g., above 10% overrun on a line item)

- Methodology: Use the Earned Value Analysis to relate not just costs but also performance progress.

- Tooling: Modern project management software makes the plan-vs.-actual comparison an ongoing process rather than a manual effort.

What happens if the budget is exceeded anyway? You’ll find answers in our article on avoiding budget overruns.

Cost Estimation Methods

The quality of the budget stands or falls with the quality of the cost estimate. Five methods have proven effective in practice — depending on the project phase and available data.

| Method | Approach | Accuracy | Best Used When |

|---|---|---|---|

| Bottom-up estimation | Estimate costs per work package and sum them up | High | A detailed WBS is available |

| Top-down estimation | Set total budget and distribute across work packages | Low–Medium | Early phase, fixed budget ceiling |

| Analogous estimation | Compare with similar completed projects | Medium | Historical data from previous projects |

| Parametric estimation | Cost per unit × quantity (e.g., hourly rate × hours) | Medium–High | Recurring, well-measurable tasks |

| Three-point estimation | Best case, worst case, most likely → weighted average | Medium–High | Uncertain projects with high variance |

Bottom-up estimation delivers the most accurate results, but requires a detailed work breakdown structure. In the early phase, when the WBS doesn’t yet exist, analogous estimation based on comparable projects is a pragmatic starting point.

The proven strategy: bottom-up as the primary method, analogous estimation as a cross-check. If the two results diverge significantly, a more detailed analysis of the differences is worthwhile.

Project Budget — Practical Example

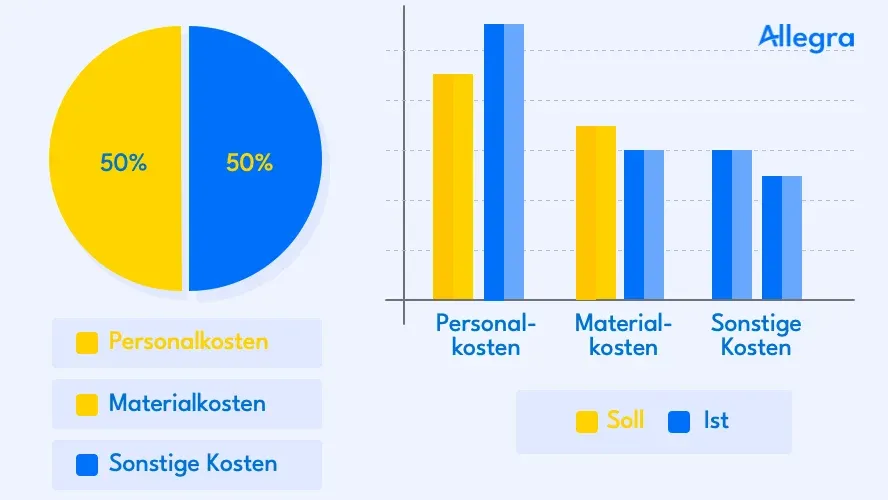

A mid-sized company plans to introduce new CRM software. Duration: 6 months. The project team consists of three internal employees, supported by an external CRM consultant. Cost estimation is performed bottom-up based on the work breakdown structure.

| Line Item | Calculation | Estimated Cost |

|---|---|---|

| Internal personnel costs | 3 employees × 60 days × €600/day | €108,000 |

| External CRM consultant | 20 days × €1,200/day | €24,000 |

| CRM licenses (year 1) | 50 users × €30/month × 12 months | €18,000 |

| Data migration | External service provider, fixed price | €8,000 |

| Training | 2 days, 25 participants | €6,000 |

| Hardware/infrastructure | Server upgrade, test environment | €4,000 |

| Travel and workshop costs | Kick-off, alignment meetings | €3,000 |

| Subtotal | €171,000 | |

| Contingency reserve (10%) | €17,100 | |

| Total budget | €188,100 | |

The contingency reserve was deliberately set at 10%: the risk analysis had identified data migration as a critical risk — legacy data in various formats could require significant rework. The budget was approved by the steering committee, and the contingency reserve was assigned to the project manager, who can release it as needed.

Template: Project Budget

The following template can be used as a starting point for your own budget planning. Adapt the cost types to your project size and industry.

| Field | Content |

|---|---|

| Project name | [Name of the project] |

| Project manager | [Name] |

| Budget period | [From – To] |

| Approved by | [Name/Committee, Date] |

| Cost Type | Estimated | Approved | Actual | Variance |

|---|---|---|---|---|

| Internal personnel costs | [€] | [€] | [€] | [€ / %] |

| External personnel costs | [€] | [€] | [€] | [€ / %] |

| Material costs | [€] | [€] | [€] | [€ / %] |

| External services | [€] | [€] | [€] | [€ / %] |

| Travel/training costs | [€] | [€] | [€] | [€ / %] |

| Overhead costs | [€] | [€] | [€] | [€ / %] |

| Contingency reserve | [€] | [€] | [€] | [€ / %] |

| Total budget | [€] | [€] | [€] | [€ / %] |

Tips for a Realistic Project Budget

Estimate bottom-up, cross-check top-down. Bottom-up estimation delivers the most accurate results because it is based on concrete work packages. The top-down perspective reveals whether the sum of the parts fits the overall picture. If the two approaches diverge significantly, something is off — and that’s exactly what you want to know before the project starts, not after.

Use historical data. Completed projects are a goldmine of cost data. How did actual costs compare to estimates? Where were there overruns, and where were there savings? Lessons learned from previous projects are the best data basis for realistic budgets.

Plan reserves — don’t cut them. The biggest mistake in budget approval: the contingency reserve is cut as “unnecessary” to make the budget look more attractive. Projects without a buffer run into trouble at the first deviation from plan. A realistic reserve is not a sign of poor planning — it is a sign of professional project management.

Think budget and schedule together. A budget is not just a total sum, but a timeline. €100,000 over twelve months requires a different cash flow plan than €100,000 in the first three months. Linking the budget with the schedule makes both plans more realistic.

Monitor regularly. A budget that disappears into a drawer after approval is worthless. Only through regular plan-vs.-actual comparisons does the budget become a control instrument. Monitoring should be part of every status meeting — not only when money gets tight.

Use PM software. Manual Excel spreadsheets are error-prone and quickly become outdated. Modern project management software already captures costs, time, and progress — the plan-vs.-actual comparison can then be retrieved with a few clicks rather than laboriously assembled.

Frequently Asked Questions

What is a project budget?

A project budget is the approved financial framework for executing a project. It encompasses all planned costs — personnel costs, material costs, external services, and contingency reserves — and is released in the project charter. The budget serves as the upper limit for resource expenditure and as the benchmark for project controlling.

What steps are needed to create a project budget?

In seven steps: (1) Clarify project goals and scope. (2) Define work packages and deliverables. (3) Identify resources per work package. (4) Estimate costs — preferably bottom-up. (5) Plan contingency reserves. (6) Compile the budget and get it approved. (7) Plan budget monitoring to detect deviations early.

What cost types belong in a project budget?

The most important components are: internal personnel costs (hourly or daily rates), external personnel costs (consultants, freelancers), material costs (materials, licenses, hardware), external services (service providers, agencies), travel and training costs, proportional overhead costs, and a contingency reserve for unforeseen expenditures.

How large should the contingency reserve in a project budget be?

The rule of thumb is 5–10% of the total budget. The exact amount should be derived from the risk analysis: projects with high technical, organizational, or external risks need more buffer than routine projects with established processes. The key is that the reserve is not cut during the approval process.

What is the difference between a project budget and a cost plan?

The cost plan is the detailed breakdown of all expected costs — per work package, resource, and time period. The project budget is the approved financial framework derived from it. The cost plan answers the question “What will likely cost how much?”, while the budget answers “What is the maximum the project may cost?” The budget is based on the cost plan, but additionally includes contingency reserves and has been formally approved by the client.

Senior Advisor

Jörg Friedrich is the original author of the project management software Allegra and continues to accompany its development to this day. He has many years of industry experience as a project and department manager. He also serves as a professor in the Faculty of Computer Science and Information Technology at Esslingen University of Applied Sciences.